Happy Independence Day! Hope you all have a great weekend.

In the first part of this series, we explored a straightforward way to save and invest for retirement, with an easy calculator to plug in your own numbers. But that was all math. There’s so much more to think about when planning your financial independence.

What can we learn from all that math?

The first lesson is no surprise: starting consistent retirement contributions as early in life as possible makes the process so much easier.

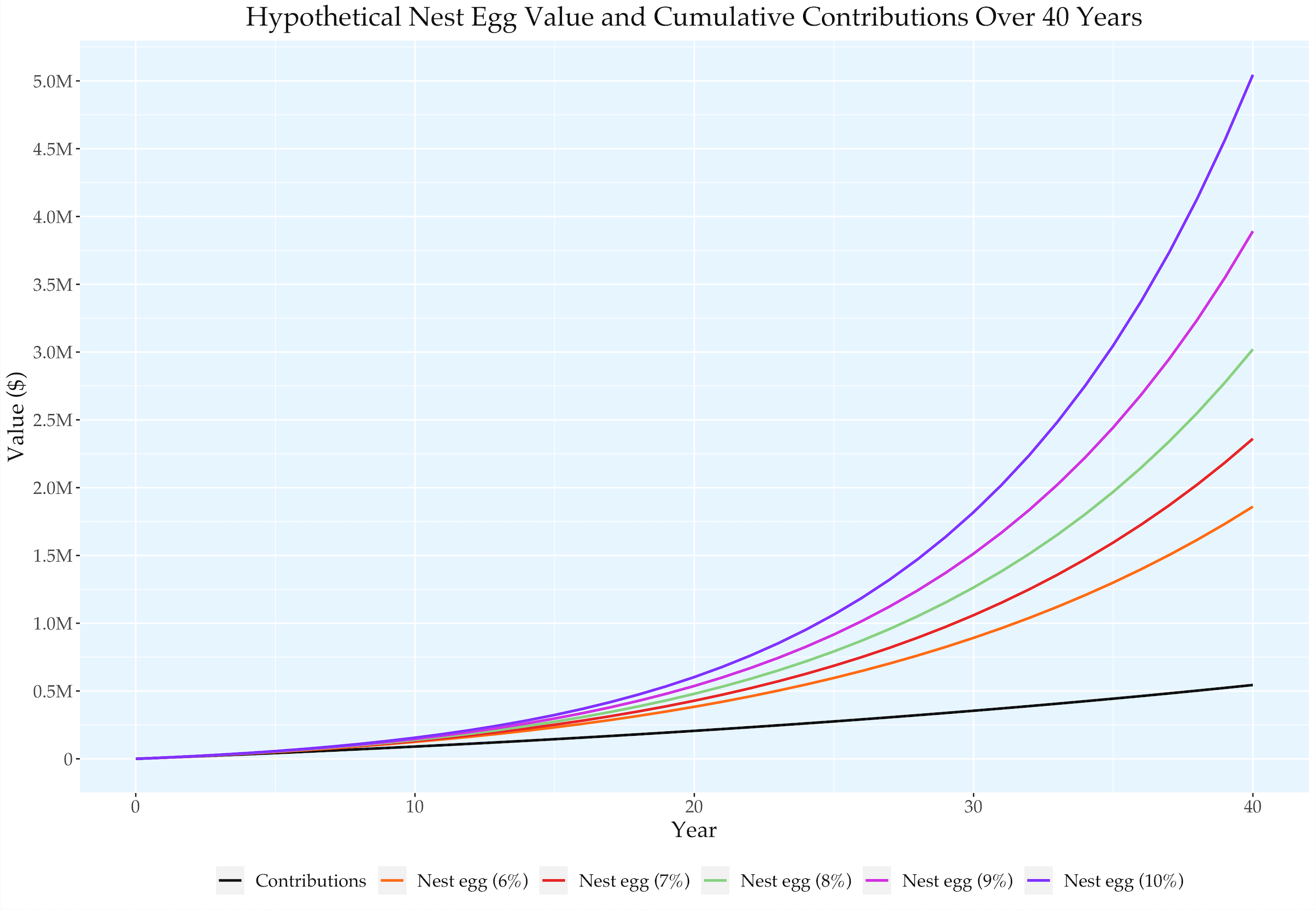

We can illustrate with the approach from our first post. We worked an example where the goal was to generate $45K of income from our portfolio, and we had 40 years until retirement. That meant we had to make an initial contribution of $8,080 in the first year. What happens without the luxury of so much time? With 30 years, the initial contribution jumps to $15,087. With only 20 years, it shoots up to $31,062. And to save for retirement in 10 years, you have to contribute $83,449 in the first year — good luck.

When you start late, you give your capital less time to appreciate. On top of that, you leave a lot more to chance. The experience of someone with only 10 or 15 years to invest will be strongly influenced by idiosyncratic trends and events; their results may be fantastic or underwhelming. Someone investing in the cap-weighted US market from 2000-2009 would’ve been deeply disappointed, whereas someone investing from 2010-2019 would’ve experienced a dazzling run-up. The average return of someone with a timeline of 30 or 40 years is more predictable.

Of course, many people cannot save large amounts of money at a young age. The point here is not to wag a finger at them, but to emphasize the importance of investing as early as possible within the constraints of your situation.

Now take a look at the graph above, from the previous post. Even a 1% difference in the average return leads to an enormous difference in lifetime wealth. If your savings habits are greater than in the example, the dollar amounts just get bigger. I don’t say this to encourage extreme risk-taking in the pursuit of higher returns. But there are three free lunches that increase your expected return: minimizing tax, minimizing fees, and increasing diversification. And while too much risk can be harmful, you should also avoid excessively low levels of risk for assets with long time horizons.

The wealth disparities also highlight why it’s important to have realistic expectations for investing. A popular book called The Simple Path to Wealth uses 11.9% as the default expectation for stock returns. Dave Ramsey, a popular author and speaker, often cites 12% as a reasonable expectation for stock returns.

Let’s put that into perspective: in our main example from the first post, the goal was a $45K portfolio withdrawal each year. We calculated an initial contribution of $8,080 by assuming an 8% return. If we predicted a 12% return instead, our initial contribution would be $2,835. That would be fine if we did get such high returns. But if we made those low contributions and ended up with 8% annual returns, that would give us an income of $16K per year in retirement — barely one-third of our goal. Is it possible to realize 12% stock returns over multiple decades? Yes, and that would be great. But your ability to retire shouldn’t depend on it.

Finally, if your spending closely matches your income throughout your working life, you’ll appear to be living within your means. But failing to save for an eventual goal of financial independence means that the appearance of spending responsibly is superficial. An ever-deepening well of investments is not only necessary for retirement: it gives you the freedom to not rely on the next paycheck to sustain your lifestyle. The ability to make decisions without the pressure of imminent financial need is one of the great rewards of building wealth. There’s a lot more to investing than maximizing your wealth at age 70.

More to consider

(1) Some people are distressed by the inherent uncertainty of retirement planning. How could you possibly know how much you’ll want to spend in 30 or 40 years? Yes, you’ll want to give yourself room to spend a lot of money on health care. But the best approach won’t involve careful research and detailed projections about future spending. You can just pick a reasonable number for now, and adjust your assumptions in the future! Your standard of living will hopefully rise as you get older, and you may want to invest more so that you can maintain your spending in retirement. Reassess your plan occasionally, while accepting that you don’t know what your life (or the world) will be like in 30 years.

(2) Annual savings targets like $8,080 don’t all come from your paycheck. Employer contributions in your work retirement plan might account for hundreds or thousands of dollars, depending on your income and their contribution policy. Once you add your own contributions, this minimum 401(k) activity can put a large dent in the savings you need. Some employers also contribute to your HSA, which can be used partly as a retirement account.

(3) We assumed a retirement portfolio of 100% stocks. Many people can’t psychologically tolerate that volatility, even in a retirement account they won’t touch for 20 years. So they allocate partly to less volatile assets like aggregate bond funds. If you do that, projections for your portfolio’s long-term growth need to be lowered accordingly.

(4) Your retirement plan should be robust: it shouldn’t collapse if stock returns are only 7% — or even less! — during your working years. If returns fall short, you may have to be prepared to work longer, increase your withdrawal rate, or decrease your spending. “Plan B” actions can include part-time work; reducing large expense categories like restaurants and certain kinds of travel; leaving a smaller bequest to children or charity; moving into a smaller home or to an area with lower cost of living; and forgoing major luxuries like a boat, a second residence, or expensive vehicles.

The best way to avoid making compromises like these is to save to a degree that you hope is excessive, and invest with modest expectations. Give yourself the capacity to be flexible: don’t fixate on a precise retirement date, or rely on above-average investment returns to meet your basic goals.

However, some ways of making money are not compromises. Working part-time or making money outside of a regular job can be a marker of success. And you don’t need to wait until you’ve built a multi-million dollar nest egg — you could plan a mini-retirement or a career downshift at any age. Personally, even working 30 hours a week is a different universe of experience for me than working 40+ hours.

(5) Taxes are an essential part of retirement planning. Your expected return could be 8% before tax, but if you’re investing in a taxable account, gains are undercut every time they’re realized. The best way to avoid tax is to hold most of your retirement investments in tax-advantaged accounts. Money in your traditional IRA is pre-tax, so using withdrawals from a traditional IRA to generate a $45K “income” is very different than doing the same with a Roth IRA. The best approach for nearly everyone is to use a combination of Roth and traditional accounts.

Wisdom to know the difference

Your plan will inevitably need to evolve as expectations change for your earnings, your standard of living, and everything else in life. There will always be factors beyond your control. Some of them are:

Asset class returns, like the returns of stocks or Treasury bonds.

Inflation rates.

Interest rates.

Federal tax rates.

Government programs like Social Security and Medicare, which may change by the time you retire.

Worrying about inflation is stressful because there’s nothing we can do about it. We can accept that we have no control over these variables, and not waste energy being anxious about that. We can instead choose to concentrate our efforts where we have a great deal of influence:

Income during your working years and changes in income over time.

Allocation and timing of investments.

Use of tax-advantaged accounts.

Use of insurance.

Where you live.

At what age you may merge finances with a long-term partner.

At what age you may have children.

Support you expect to provide to and receive from your family.

How much you’ll spend, save, and invest during working years.

How much you’ll change your spending during retirement.

How you’ll change your investment approach during retirement.

Age of retirement.

Whether you retire suddenly or continue earning a smaller income for some time.

Personal goals such as charitable donations or leaving money for your children.

We can find a sense of control by keeping our own house in order.

What’s up with Social Security?

There are multiple programs run by the Social Security Administration. When people think of “Social Security”, they’re usually referring to the Old-Age and Survivors Insurance (OASI) program, which has over 60 million benefit recipients. Americans can apply to start receiving old age benefits between ages 62 and 70. Benefits are paid monthly in cash, and they’re adjusted for inflation annually.

Social Security is funded by payroll tax as well as income tax on Social Security benefits. Any excess funds not immediately paid out are held in a trust fund, so another source of funding is the interest earned on the trust fund reserves.

The latest report projected that if Congress makes no changes to OASI, the trust fund will be depleted in 2033. After that, benefits will automatically drop to about 77% of the scheduled amounts. Social Security benefits will always be funded by ongoing tax revenue, which means they’ll never disappear completely unless Congress passes a law to that effect. The only question is whether Congress will mobilize enough dollars to pay benefits in full.

Without a doubt, Congress will make some changes to OASI before 2033. There might be a combination of benefit reductions and tax increases. But we can’t know exactly what those changes will be. So as a conservative plan for retirement, we can anticipate receiving three-quarters of our scheduled benefits.

Okay — but how do I know what my scheduled benefits are? There are several official calculators, including a simplified calculator with only a few inputs, and one that lets you enter your past earnings.

An easier approach might be to think in terms of replacement rate: what portion of my income will be replaced by Social Security? Reports like this one have shown that the median American receives about 40% of their pre-retirement income from Social Security. If you think you’ll spend 80% of your prior income in retirement, that’s about half of your retirement income from Social Security.

However, Social Security is a progressive system: a low-income American could receive benefits that replace 80% of their prior income, while a high earner’s rate might be only 20%.1

That’s one reason why replacement rates aren’t the best way to plan for Social Security. If you’re within a decade of retirement, you should create a “my Social Security” account and check your projected benefits based on your actual earnings history. But if you’re many years out from retirement, you can get a rough estimate based on replacement rates or the simplified calculator. With an average individual income — which was $66,600 in 2023 — it’s reasonable to assume that your scheduled benefits might replace 40% of your income. But depending on Congressional action, that could be as little as 30% due to the funding shortfall. To reach a total of 80% of prior income, you would need to build a retirement portfolio from which you can withdraw 50% of your income.

As with your investment outcomes and your future spending, your estimates of Social Security benefits won’t be perfect, and that’s FINE. Take a deep breath, pick a reasonable number, and reassess every once in a while.

Rules of thumb

Are there any guidelines that quickly approximate the right way to save for retirement? The first one is quick because it’s so bad. Fidelity has featured a guideline on their website for years, which expresses retirement savings as a multiple of your current income. They suggest having:

1x your income by age 30

3x your income by age 40

6x your income by age 50

8x your income by age 60

10x your income by age 67

There are others like it, but Fidelity’s prominence has given this one a lot of reach. An obvious issue is that it attempts a one-size-fits-all solution. Maybe this could be sensible for someone who started working at 22 with a bachelor’s degree, and has a smooth upward career path. For a specialized physician with a negative net worth at 32 but very high earning potential, it’s nonsense that has the potential to promote anxiety and confusion. Feeling financially “behind” is a common panic-inducing emotion that can lead to poor decisions. I don’t think this is a good rule to broadcast to the public with few caveats.

However, the final number — 10x your income at age 67 — isn’t a bad rule of thumb for the average American. How do we know? In the section above, we mentioned that the median American receives about 40% of their pre-retirement income from Social Security. They would need another 40% from their portfolio to reach typical retirement spending levels.

Let’s pick a $50K income, for the sake of a round number. 40% of that would be $20K. Assuming they withdraw about 4% of the portfolio each year, how much money would they need to generate an “income” of $20K?

Hey, it’s 10x their income!

On top of the other issues, this guideline lacks one of the crucial numbers people want — how much do I invest each year?

That brings us to another proposed rule. What about “save __% for retirement”? By far the most common suggestion I’ve seen is to save 15% of your pre-tax income for retirement. Is that the right amount?

Okay, again we have the problem of trying to fit everyone into a single guideline. But let’s find someone for whom 15% does make sense! We’ll use $100K as pre-retirement income. Let’s say they want a portfolio that generates $40K per year in today’s dollars, supplemented by Social Security. We enter 30 years and $40K into the calculator and find that the first year’s contribution is $13,411, or about 13.4%. That’s not far from 15%! And saving a little more would leave them a good safety margin in case returns are lower than expected.

So it works for someone who expects 40% income replacement from Social Security and has 30 years to save for retirement. But the same person with only 20 years would have to save 28% of their income. On a breezy timeline of 40 years, they would need to save only 7%. Or if they had 30 years but expected less from Social Security, they would need to compensate by saving more.

“Save 15%” is not the worst rule of thumb. It’s dead simple and would actually work for many people. Let’s improve it a little without making it complicated! If you’re starting with zero retirement investments:

Save 8% if you have 40 years.

Save 15% if you have 30 years.

Save 30% if you have 20 years.

Of course, there’s no substitute for running your own numbers. I made that as easy as possible with the calculator and spreadsheet from our first post. And I think people gain a lot more satisfaction and confidence by making their own decisions, rather than blindly following a rule of thumb that supposedly applies to everyone.

—

I hope that was helpful! See you next week.

Further resources

Every Money IRL post is organized in The Omni-Post, and all vocab terms are here.

I recommend this interview with financial advisor Michael Kitces on a variety of retirement topics. Among several other ventures, he helps retirees for a living!

You can see the national average wage in each year calculated by the Social Security Administration here.

Check out the gentle intro to investing for more info on investing for retirement and other goals.

—

We love comments here. Tell us what you like or dislike, agree or disagree with. Recall a long story barely related to this post. Ask a question!

Please send photos of your pets if you’d like to see them in future posts. Or suggest a new topic, or say hi! You can email or tap the message button. Stay safe out there.

Email: bright.tulip711@simplelogin.com

—

That’s partly because the federal payroll tax that funds OASI benefits has an income cap. Those who earn more than the cap — $176,100 in 2025 — don’t contribute any of their income above that threshold to Social Security. As a result, they don’t get any Social Security benefits to replace the income above that threshold. Of course, we’re talking about high earners and they should be able to easily self-fund their own retirement with some basic planning.

This was my favorite post so far because I’m newly financially self sufficient and saving for retirement for the first time.