The easy parts of estate planning

In case you step on a box jellyfish.

Estate planning is the process of legally and logistically preparing for your death, as well as potential incapacity before death. It can be daunting even for financially literate people, with jargon like “probate” and “irrevocable trust”. We’ll start with a few simple actions that everyone should take regardless of their assets or life expectancy. Why does estate planning matter?

Think of estate planning as an obligation to your loved ones

Many people don’t put a moment’s effort into preparing for their death because they intend to live for many more years. When such people die suddenly, some of their loved ones are thrown into a confusing process. On top of grieving, someone is charged with figuring out where their assets are located, whether they had life insurance, and how to navigate the legal fallout of a person who died without indicating what should happen to their children, their pets, their assets, their possessions, and their own bodily remains.

Even if the deceased had a complete estate plan at one point, they may have neglected to update it and accommodate changes to their wishes or the estate itself. Everyone dies, and many people die suddenly in car accidents, homicides, medical emergencies, and natural disasters every day. They weren’t expecting it. Your premature death would be hard enough for your loved ones: you can make it slightly easier by creating an estate plan — even a rudimentary one — and occasionally reviewing whether it’s up to date. There may never be a time at which these tasks announce themselves as urgent, which is why some people die before getting around to them. You can read this post and start right now. If there are people whose estate planning (or lack thereof) would affect you upon their death — such as your spouse, parents, or siblings — you may want to help them complete the tasks described below.

The easy parts

An estate plan can be started by making an informal “in case of death” document that your loved ones can access. It’s often called a “letter of intent”, but I’ll just call it your estate planning document. The document should contain everything you would want to communicate if you died suddenly. At a minimum, it should list each institution that custodies your financial accounts; valuable physical items that you own; any debt that you owe, including credit cards even if you pay them off every month; info needed to file your tax return; and any directions that don’t need legal force, such as wishes for disposal of your remains. Include the account number with each account, loan, or credit card.

If you own a home, you may want to describe how and when you pay the utilities, property tax, insurance, and mortgage (if any). That would make it easier to care for the home, even if it would be put up for sale right away. If you have a tax preparer, attorney, or financial advisor, their name and contact info should be added. If you have a product with survivor benefits, like life insurance or a joint and survivor annuity, it should be included as well. Don’t forget about life insurance you may have through your employer. Creating a document like this is often part of building an estate plan with an attorney, but everyone can and should do it on their own.

This document makes all the other steps easier. Where should you keep it? A Google Doc with shared viewing permission works well, since you can update it anytime, it can be easily accessed by others, and it can’t be physically destroyed by a fire or flood. Some people keep the document on paper. This allows them to potentially keep the information private until their loved ones access it. But a paper document is physically vulnerable, harder to update, and more likely to be misplaced or become inaccessible to your loved ones. Once they need it, it’s too late to remind them where you keep it or how to open your safe. What if you want to keep your document private, but ensure that it’s easy to update and accessible at the right moment?

Personally, I use Bitwarden’s trusted emergency contact feature. Bitwarden is an end-to-end encrypted password manager, and my estate planning document is stored in Bitwarden’s secure notes. My trusted contacts can request to view (but not edit) my account, and as long as I’m not around to deny the request, they’ll gain access after a period of time I selected. This allows me to disclose information I wouldn’t want to share while I’m alive, like my account passwords and the passcodes to my phone, computer, and safe.

As you could guess from the barrage of photos on this Substack, my estate planning document has detailed instructions on how to take care of my cats. They have specific diets and a list of medical needs, and I would want them cared for even if my partner and I died together in a car accident. Most people don’t have a plan for their pets (or even their children) if something like that happened.

The first task has given you a convenient list of all your financial accounts. The next easy win is to designate beneficiaries for each account. The beneficiaries you name will determine who inherits your assets. These include bank accounts, brokerage accounts, retirement accounts, health savings accounts, employee ownership programs, US Treasury savings bonds, and life insurance (both individual and employer-sponsored policies). A beneficiary can be a person or an entity (such as a charity).

Many accounts provide an option to name two sets of beneficiaries: primary beneficiaries — who inherit the account by default — and contingent beneficiaries, who typically inherit nothing but would inherit the account if all primary beneficiaries pre-deceased you (i.e., they were already dead at the time of your death). For each set, you can name one or multiple beneficiaries, and dictate the share of the total paid to each. If an account offers the option to add a per stirpes designation, that would leave a beneficiary’s share to their children if that beneficiary pre-deceased you.

Your beneficiaries should be mentally competent adults. If you’d like to leave assets for the benefit of someone who doesn’t meet that description — most commonly your minor children — an estate planning attorney can help you develop a customized arrangement.

Bank accounts usually have “payable on death” (POD) designations that are more limited. Many banks allow you to name only a single beneficiary on each account. Some banks, like Chase and Wells Fargo, require that you visit a branch to name your beneficiary. Others, like Capital One and Bank of America, let you do it easily online. Although it’s not a universal practice, you can usually confirm that your bank account has a beneficiary by checking your monthly statements: instead of printing only your name at the top, it will typically read “[Your name] POD [Your beneficiary’s name]”.

You can include the beneficiary of each account in your estate planning document:

Little Bank of the Shire

Checking account - 123456789

Primary beneficiary is Frodo Baggins.Savings account - 987654321

Primary beneficiary is Samwise Gamgee.https://www.littlebankofshire.com

If the beneficiaries you choose to name might be confusing or surprising to some of your loved ones, it can help to explain your decisions in the document. Or you may want to pro-actively explain your choices while you’re alive. Of course, most people’s estate plan choices are simple and don’t require much explanation.

Jargon break

An “estate” can mean a large fancy property but, in this context, every adult has an estate. Your estate is the sum of your financial life: all your assets and liabilities.

Assets are the positive part of your balance sheet. Anything with a positive market value is an asset, including financial accounts like a checking account, as well as valuable physical possessions like a car.

Liabilities are the negative part of your balance sheet. A liability is an amount owed. Debt is the most prominent liability for most people, but it’s not the only kind. A mortgage payment due in two weeks is a liability, but so is a rent payment due in two weeks, even though rent isn’t debt. A tax bill due in three months is a liability as well.

Now back to the show.

Last will and testament

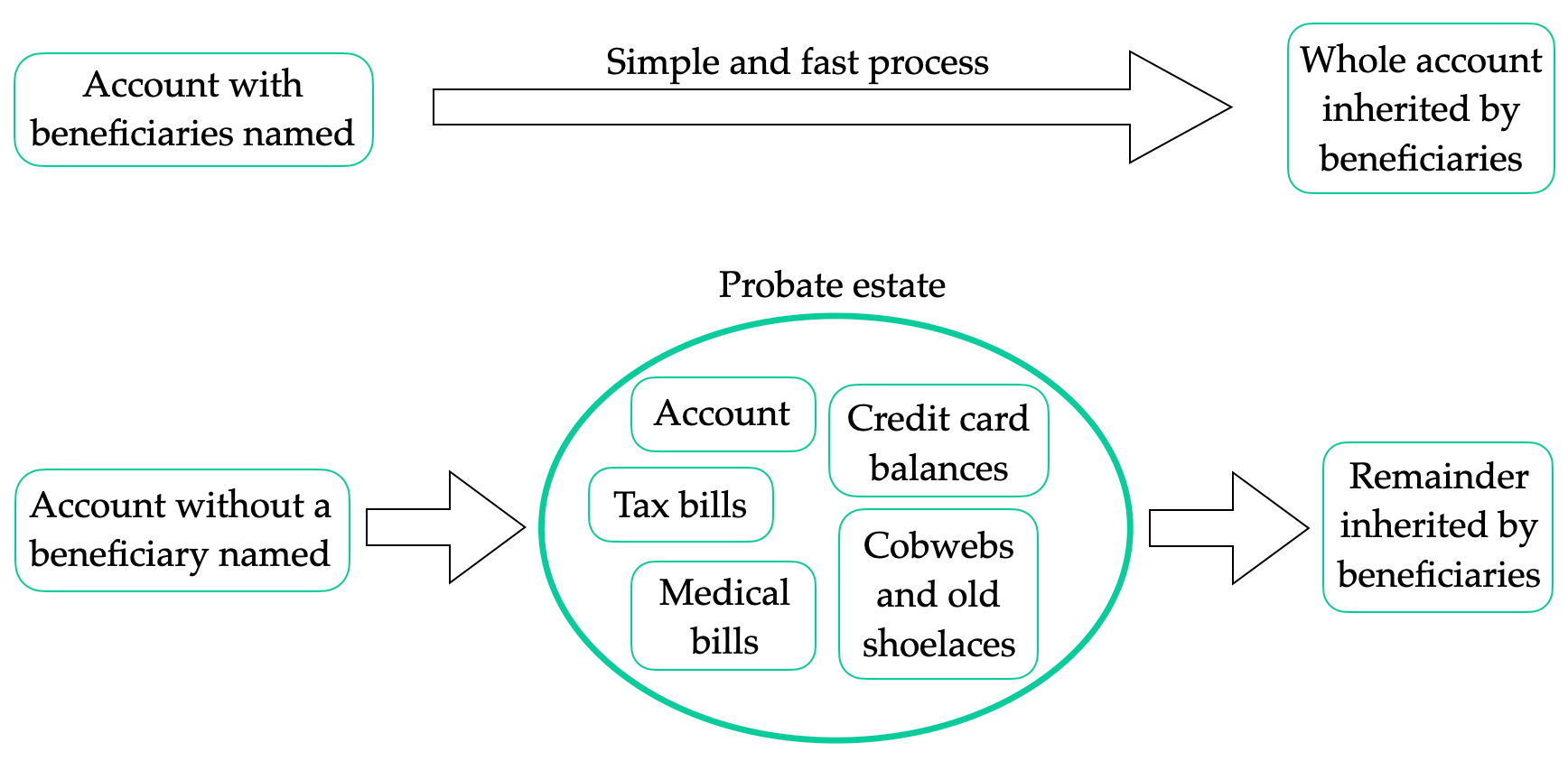

What about your last will? Doesn’t that matter? Sometimes it’s less important than everything we covered so far. Inheritance of most financial accounts is completely handled by naming beneficiaries, as long as they’re still alive when you die. Those accounts would be promptly transferred to your beneficiaries once they present each institution with a copy of your death certificate. Not only do you not need a last will for that, but beneficiaries named on an account supersede your last will. If the bulk of your net worth is in financial accounts and you decide to follow the recommendations above, then congrats! You’ll have already finished the most significant part of your estate plan.

The rest of your property may enter probate when you die. Probate is the legal process in which your assets are inventoried, liabilities are settled, and any remaining assets are transferred to your heirs. If you died with a valid will, it would dictate the probate process within the bounds of state law. You can name the beneficiaries of your estate, and the executor who would manage the estate during probate. If you did not have a valid will, you died intestate (think “without testifying”). Because you didn’t declare (with legal force) how your estate should be handled, state law would govern who benefits from your probate estate.

Probate can be expensive, especially if family members clash over their rights to the estate. It takes a long time — months or occasionally even years. So a common goal when people work with an estate planning attorney is to ensure that their major assets bypass probate, or even to avoid it altogether. Creating a last will doesn’t let you avoid probate; it merely guides probate.

Some states have made it easy to name beneficiaries of assets beyond financial accounts. Depending on your state, you may be able to register your vehicle with a “transfer on death” (TOD) beneficiary. TOD is similar to POD for bank accounts, but of course a car isn’t “payable”. If you own your home in a state that permits a TOD deed, a beneficiary can be named and the property would bypass probate.

Naming a beneficiary for your home is simple if you’re the sole owner. What if you’re not? Most people in the US who buy a home together are “joint tenants with rights of survivorship”. When one joint tenant dies, the others inherit equal portions of that share of the property. Most commonly, Spouse X and Spouse Y own a home as joint tenants. If Spouse Y died, Spouse X would automatically inherit their share, becoming the sole owner. Spouse Y might have a last will, but it doesn’t apply here. They could leave their entire estate to Charles Entertainment Cheese, but it wouldn’t affect who owns the home.

These laws apply regardless of whether the joint tenants are married. If Girlfriend A and Boyfriend B were joint tenants, and Girlfriend A died, Boyfriend B would automatically inherit her share. What if the property has a TOD deed? In this case, a beneficiary of the deed wouldn’t inherit anything. All joint tenants would need to die before the beneficiary kicks in. The same applies to beneficiaries of joint bank accounts and joint brokerage accounts.

Can debt be inherited?

Thankfully no one has to fear being saddled with involuntary debt. You can choose to inherit certain debts because they’re attached to an asset like a vehicle or real estate property.

During probate, the estate’s assets and liabilities are compiled, and the liabilities are settled before dispersing assets. If the assets exceed the liabilities, the estate beneficiaries inherit the remaining assets. If the liabilities exceed the assets, the beneficiaries may receive nothing. But unsecured debts and other liabilities are not inherited, and the creditors who weren’t fully repaid have to pound sand. Unsecured liabilities include student loans, credit card debt, tax bills, and unpaid medical bills (possibly incurred shortly before death).

On the other hand, you’ll be responsible for continuing the loan payments if you inherit a home with a mortgage loan, or a vehicle with an auto loan. Those loans are secured against collateral — the home or vehicle. If you can’t afford to service the loan, you might need to sell the asset to pay it off. If you don’t want it in the first place, you’re not obligated to accept property that you inherited: you can disclaim it.1

Debt is a crucial reason to minimize your probate assets. If you have (say) a brokerage account with named beneficiaries, that account would be transferred to the beneficiaries and could not be used to settle your unrelated debts. But if you failed to name a beneficiary, the brokerage account would become part of your probate estate upon your death. If there were liabilities in your estate that would have otherwise gone unpaid, the brokerage account could be drained — partially or completely — in order to satisfy those liabilities.

That was easy … so far

Creating your estate planning document, making it available to your loved ones, and naming beneficiaries are pretty easy tasks. You should refresh your document and evaluate your beneficiaries at least once a year. There are pertinent events that should also remind you to check your estate plan: marriage or divorce, a birth or death in the family, buying or selling valuable items like real estate, opening or closing an account, moving out of state, changing jobs along with benefits like life insurance, or a relevant minor in the family becoming an adult.

Updating your beneficiaries ensures that your estate plan would play out as you intended. If any of your beneficiaries pre-deceases you, that could cause assets to inadvertently land in your probate estate.

On top of that, we discussed potential ways to keep your real estate and vehicles out of probate. It’s great that some states have made it easier to minimize probate assets without a lawyer. It’s even possible to write your own last will. But you probably can’t build a full estate plan on your own. A good estate planning attorney isn’t there to just translate your wishes into legal documents. They can inform you about the landscape of challenges and options, and might call your attention to issues that you hadn’t considered.

In future posts, we’ll discuss the problems you can solve through estate planning, the available tools beyond a last will, and how to position your investments with estate planning in mind. See you next week!

Further resources

Every Money IRL post is organized in The Omni-Post, and all vocab terms are here.

Paul Rabalais is an estate planning attorney with a great YouTube channel. He has a ton of videos and livestreams covering so many aspects of estate planning. His video on avoiding probate that I linked above is an excellent summary, although it uses jargon that wasn’t introduced here. He has another video describing a probate in detail, and here are a couple videos on selecting an executor for your estate. If you want to learn more about estate planning, you could start by listening to a bunch of his videos.

The Retirement Nerds run a YouTube channel focused on Social Security, Medicare, and estate planning. Here’s a video summarizing how to plan for incapacity, and here’s a detailed interview with an attorney about the highlights of an estate plan.

You can read about the different ways to hold the title of a home here. We discussed joint tenancy and sole ownership above. Read about TOD deeds for a home here, and about registering your vehicle with a beneficiary here.

Check out our post on life insurance, which is a critical part of estate planning.

—

We love comments here. Tell us what you like or dislike, agree or disagree with. Recall a long story barely related to this post. Ask a question!

Please send photos of your pets if you’d like to see them in future posts. Or suggest a new topic, or say hi! You can email or tap the message button. Stay safe out there.

Email: bright.tulip711@simplelogin.com

—

You may want to disclaim an asset if it’s worth less than the loan secured against it; this is referred to as being “underwater” on a mortgage or other loan. But that’s not the only option: do your research — and possibly, consult an expert — before disclaiming. Another reason to disclaim is that you’d like to deliberately pass the inheritance to the person who’s next in line. Perhaps for tax reasons, a person whose spouse just died might disclaim an account, allowing the contingent beneficiaries (their children) to inherit it.

Great article!