You have

debt

extra money

And you want to put that money to work. How do you decide whether to invest the money or make additional payments on your debt? Is there even a correct answer, or is it mostly subjective?

All models are wrong, but some are useful

In our post on how to rent from a homeowning partner, we discussed how to compare the costs of renting and owning a home. In some important ways, renting and buying are incommensurable — they can’t be strictly compared on a common measuring stick. But for practical purposes, we can bridge the gap by estimating the total explicit and implicit costs. There are a bunch of caveats, and that’s okay.

Paying debt (beyond the minimum payments) saves you money by reducing interest, with no risk of losing money. Investing can generate positive earnings, but usually carries some degree of risk. They can both increase your net worth, which is the space where we’ll build a rickety bridge between the two activities. Hypothetically, you could attain the same net worth increase by (a) making extra debt payments or (b) investing that money.

More generally, we can say:

Paying debt with a fixed interest rate is roughly equivalent to buying a tax-exempt investment with a guaranteed return equal to the interest rate.

Paying a credit card balance with a 28% interest rate is like investing that money and earning a risk-free 28% annualized return. With no tax! Throw in a few asterisks that we’ll explore later. Despite imperfections, it’s a good framework for relating debt payments to investing.

Let’s walk through an example. First: in our quick overview of tax basics, I warned you that you’d need to know about marginal tax rates to understand this post. Check out the tax post or this video if you need info about marginal tax rates.

We have two loans that we’d like to compare to investing in our taxable account. Our student loan has an interest rate of 7%, and our mortgage has a rate of 3%. If we follow the statement above, payments on the student loan are like a tax-exempt, risk-free investment with a 7% annual return. How do we compare that to buying a taxable investment?

Let’s say that for federal income tax, our marginal rate is 22% for ordinary income (like from our job) and short-term capital gains. Our marginal rate for long-term capital gains is 15%. Both of these are very common rates. We live in a made-up state that taxes both short-term and long-term capital gains at a flat rate of 5%. So we add federal and state tax to find total marginal rates of 27% (22+5) and 20% (15+5).

We expect the investment earnings to largely be taxed as long-term capital gains, since we’ll buy stock ETFs. So we’ll assume a 20% marginal rate. If we posit that the after-tax return is 7%, what’s the pre-tax return? .07/(1-.2) = .0875, giving us a pre-tax return of 8.75%. In other words, 8.75 becomes 7 after losing 20% to tax.

We can do the same with the mortgage: .03/(1-.2) = .0375. 3.75% is the pre-tax gain, which becomes 3% after tax.

Wow, that was easy: paying our student loan is equivalent to buying a taxable investment with a guaranteed annual return of 8.75%. That’s a great deal by almost any standard. 3.75% is a clear contrast: higher potential investment returns are out there, so if we’re comfortable with risk, we may want to make the following plan:

Focus on paying off the student loan as soon as possible.

Once that’s done, start investing our extra money.

Keep making minimum payments on the mortgage to maximize step 2.

Is that all? We just place debt payments into the menu of possible investments, and use that to decide if we want to make extra payments? Not quite: there are some asterisks.

Paying debt reduces liquidity

If we used our extra money to buy shares of a stock fund, we would own a liquid asset that we could choose to sell on short notice if needed. Yes, the value would be volatile and could fall below the initial value, but the shares would always be an asset with some value. If we instead paid off debt, we couldn’t reverse that decision easily. We’d have to borrow the money again to get it back. That’s much harder, and we may not be able to borrow on the same terms — they’re not giving away 3% mortgages anymore!

Retaining the asset on your personal balance sheet is a point in favor of investing.

Paying debt isn’t always tax-neutral

So far we assumed that paying debt — and reducing interest — is similar to a tax-exempt investment. But interest can be tax-deductible! This effectively lowers the interest rate of the loan, making it less attractive to pay down.

Up to $2,500 of student loan interest each year is tax-deductible, as long as our income is low enough. We already know that our marginal rate for ordinary income is 27% across federal and state tax. So if our interest in a given year was fully deductible, taking the deduction would reduce our interest bill by 27%. Subtracting 27% from our 7% interest rate gives us a 5.11% effective rate. If we want to compare that rate to a taxable investment, we subtract 27% from our previous rate of 8.75%, giving 6.39%.1

By considering the effects of tax on both investments and debt payments, we’re able to compare them more fairly. Under these assumptions, paying a 7% student loan with fully deductible interest is similar to a taxable investment with a guaranteed 6.39% return, not 8.75%. That still makes paying our student loan a good deal, but not as great as before.

If the reasoning above was unclear, you may find it helpful to check out the section on credits and deductions in the tax basics post. If you want to understand how tax deductions apply to a mortgage loan, you can check out this footnote.2 Most Americans with a mortgage don’t get a tax break from their mortgage interest, because they take the standard deduction.

The tax law passed in July 2025 makes auto loan interest deductible in tax years 2025 through 2028 for new vehicles with final assembly in the US (with income restrictions).

That’s everything on this point — don’t forget about deductions for certain types of interest!

We can invest tax-efficiently

We assumed above that a new taxable investment loses 20% of its annual return to tax because our marginal rate is 20%. That would be true if we consistently sold after holding for a year, triggering immediate taxable gains each year. But if we held for multiple years, we’d get to keep investing the unrealized gains. We wouldn’t have to hand over any tax until we eventually sold (aside from tax on dividends).

Increasing your holding period decreases the overall tax rate. We used 20% above because there’s no particular number we should choose instead. It depends on several factors. But in reality, a well-behaved investor won’t lose as much to tax as their tax rate suggests.

Investments aren’t always taxable

What if instead of paying debt or adding to a taxable brokerage account, we increase contributions to a tax-advantaged account? That would be a point for investing, but there are drawbacks. Tax-advantaged accounts restrict your ability to withdraw money by imposing tax penalties. The most notable exception is that you can withdraw the sum of all your Roth IRA contributions without triggering any tax penalties or income tax.

So if you invest more in tax-advantaged accounts, you’ll probably sacrifice some of the liquidity benefits provided by investing in your taxable account.

Beyond asterisks

There are some no-brainer situations when it comes to paying debt. At one extreme, a credit card balance earning (say) 28% interest should be paid off with urgency, almost regardless of your situation. At another extreme, let’s say you have the option to use an auto loan at a super-low promotional rate, and you can earn interest at a higher rate — even after tax — by investing in a risk-free fund like VBIL.3 This isn’t rare for borrowers with high credit scores, because lenders often use auto loans as a loss leader for customer acquisition. You could have the money to buy the vehicle in cash, but you would profit by purchasing VBIL with that cash and making minimum payments on the loan. If the yield of VBIL ever dropped low enough that paying your loan became a better deal, you could sell your shares and vaporize the loan.

To appreciate those details and still want to avoid that sort of loan, you would need a high aversion to debt. Some people value a feeling of security, including low or no debt, above other financial goals. Buying a car in cash or quickly paying off your 3% mortgage may not pencil out if you only want to maximize your expected net worth. But some people love the feeling of being debt-free, and they’re fine with not optimizing for other variables.

Other people find it difficult to invest in risky assets, because the volatility is so stressful or terrifying. If you can’t buy stocks without panic-selling when they drop, then you won’t earn their high expected return. Most bonds have a lower expected return than a broad stock fund, and bond income is taxed at a higher rate (your ordinary income tax rate).

If you have high debt aversion or high risk aversion, that’s a point in favor of paying debt rather than investing. Personally, I found that automating all my finances helped reduce both of those aversions. I wasn’t bothered much by low-interest debt or stock market volatility once I stopped regularly checking my accounts.

You may have wondered: if I consider investing in a broad stock fund, what expected return should I compare against paying debt? Since 1900, the average return of the cap-weighted global stock market has been about 8% (or slightly over 5% after inflation).4 There are some evidence-based ways to seek higher return, but I think the default number for a broad stock fund should be 8%. Of course, the “expected return” of an investment is not the return you actually expect. Stocks have a wide distribution of returns, most of which are a lot higher or lower than 8% in any given year.

Based on this info, you could reasonably make the following assumption:

If mortgage rates are low enough that I can get a 4% rate, then I should make minimum payments and invest my extra money in stocks. But if rates are higher and the best I can get is a 7% rate, then I should focus on paying down the mortgage, because a risky asset with an 8% expected return doesn't sound attractive under those conditions.

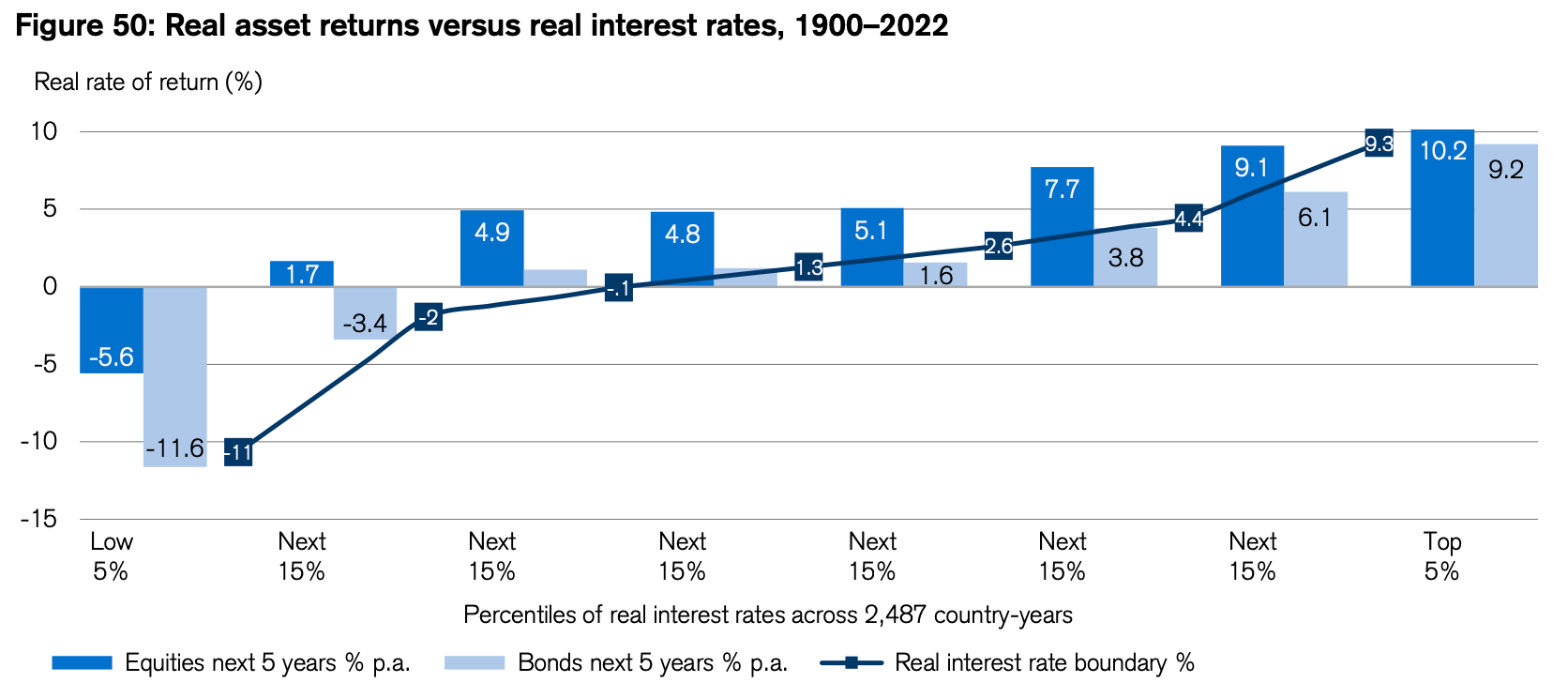

In other words, you might assume that paying debt is inherently more attractive in a higher interest rate environment. This is a questionable assumption, because expected return isn’t static: stocks have historically performed better in higher-rate environments.5 It makes sense from an investor’s perspective: when rates increase and push up the returns of lower-risk bonds, riskier assets are repriced to permit higher expected return. Investors won’t buy stocks unless their prices are cheap enough to provide a much higher expected return than low-risk bonds.

If you’ve done the math and still find yourself uncertain, splitting your money between debt payments and investing is a perfectly fine solution. Or you may think that paying debt is clearly the better move after accounting for risk, but you also want to build up assets that could be liquidated for potential spending. You certainly don’t need to invest in stocks if building up savings is your goal. At a minimum, nearly everyone should have an emergency fund even if they have debt.

There are two ways of expressing an interest rate: APR (annual percentage rate) and APY (annual percentage yield). APR is mainly for calculating how much interest you can expect in a given month. APY accounts for compound interest, so APY is the number to check for the annualized interest rate, which can be compared to the expected return of an investment (before tax). APR is always the lower number, which is why banks advertise APR for loans and APY for savings accounts. You can convert between them here. A credit card with a rate of 20% APR converts to about 22% APY.

Paying debt can be a very attractive counterpart to investing, but it’s not a purely qualitative decision based on where your vibes are pulling you that day. There are rigorous ways to consider it carefully, and the math is nothing crazy.

See you next week.

Further resources

Every Money IRL post is organized in The Omni-Post, and all vocab terms are here.

Read about the student loan interest deduction and the mortgage interest deduction at those links.

Ben Felix explains in this video why it often makes sense to pay off your mortgage instead of allocating a large fraction of your taxable portfolio to bonds. Ben Felix is a Canadian advisor, so he won’t discuss the mortgage interest deduction, and Americans can largely ignore the mentions of a pre-payment penalty or renewing your mortgage.

If you aren’t familiar with some of the terms used above, like “cap-weighted” and “deduction”, please check out the gentle intro to investing and the overview of tax basics.

—

We love comments here. Tell us what you like or dislike, agree or disagree with. Recall a long story barely related to this post. Ask a question!

Please send photos of your pets if you’d like to see them in future posts. Or suggest a new topic, or say hi! You can email or tap the message button. Stay safe out there.

Email: bright.tulip711@simplelogin.com

—

We find the same result by determining the taxable equivalent of 5.11%: .0511/(1-.2) = .0639, or 6.39%.

Student loan interest can be deducted “above the line”, which means that those who take the standard deduction can also take this deduction (if they qualify). Those who take the standard deduction cannot deduct mortgage interest from their taxable income. Mortgage interest can only be an itemized deduction.

The value of the mortgage interest deduction is harder to calculate because you have to give up the standard deduction to use it. Because everyone gets the standard deduction for free, the value provided by itemized deductions is based on how much your total deductions exceed the standard deduction.

The standard deduction in tax year 2025 for a single filer under 65 is $15,750. Let’s say a fairly high-income, single taxpayer has qualifying mortgage interest of $7,000; deductible state and local tax (SALT) of $9,000; and charitable donations of $5,000. She has $21,000 of itemized deductions, so the additional deduction gained by itemizing is $5,250. Only 25% of her total deduction is a gain relative to the standard deduction.

Since only 25% of the itemized deductions contribute to a greater overall deduction, each dollar of mortgage interest reduces taxable income by only 25 cents. With the student loan interest deduction, we determined that the effective interest rate is reduced by the marginal tax rate, 27%. We’ll use 27% here too. With this case of the mortgage interest deduction, the effective interest rate is reduced by 25% of 27%, which is 6.75%.

If her mortgage has a 3% interest rate, subtracting 6.75% from our 3% rate gives a roughly 2.8% effective rate after tax. If we wanted to compare that effective interest rate to a taxable investment, then we’d do the same math as above and subtract 6.75% from a 3.75% rate, giving us a roughly 3.5% rate.

So in this example, investing becomes even more appealing compared to paying a 3% mortgage. After accounting for tax on investments and the mortgage interest deduction, paying the mortgage is roughly equivalent to buying a taxable investment with a guaranteed 3.5% return.

So we’re done? Almost — that’s why this is in a footnote, it’s really long. Unlike the effective interest rate of a student loan, the effective rate of a mortgage is dynamic: it depends on how much you pay during each tax year. If this person had paid extra on her mortgage, she would have paid slightly less mortgage interest in that year and the mortgage interest deduction would have been slightly less valuable. Future extra payments would become slightly more attractive because that would shrink the future mortgage interest deduction (relative to making minimum payments), increasing the effective interest rate.

VBIL is the Treasury bill fund with the lowest expense ratio, making it the best and easiest way for most people to maximize their risk-free return. Nearly all savings accounts have lower pre-tax returns than VBIL, and interest from a savings account is subject to more tax. A similar fund managed by BlackRock is SGOV. For more info, check out the post on low-risk and no-risk places to keep your money.

See the 2023 summary edition (p. 15, fig. 11) of the Credit Suisse Global Investment Returns Yearbook for recent stock data showing that the average real return (i.e., after inflation) has been about 5%. The exact number varies depending on whether they report local currency returns (as in the 2023 summary edition) or USD returns (as in the 2021 summary edition), which are more relevant and have been slightly above 5%. Excluding a few periods of hyperinflation, the average inflation they find is about 2.6% (p. 16, fig. 5). These translate to a roughly 8% nominal return.

See the 2023 summary edition (p. 20, fig. 50) of the Credit Suisse Global Investment Returns Yearbook. The new reports are called the “UBS Global Investment Returns Yearbook”, because Credit Suisse was bad at remaining solvent and was acquired by UBS in 2023.

This was a really insightful article; I wish I knew you when I was younger. :) I would have avoided a lot of mistakes.

Very good article. I learned a lot