Stock & bond investing - a gentle intro (part 2)

Passive investing does not exist.

You can read Part 1 of this introduction here.

Back for more? We paused last week on the idea that we can simplify and diversify in a single step, by investing in a fund instead of individual stocks and bonds. You’re going to invest as long as you live, so it should be easy. This post is a way of thinking through how to build your portfolio.

The basic unit of equity is a share, but bonds are already the basic units — you buy individual bonds, not shares of bonds. However, fund units are always shares, whether the fund contains stocks or bonds or both. Stock funds will be the focus today.

Funds aren’t an automatic tool for simplification: there are more stock funds than individual stocks. So we need principles that help us drastically filter down the options. The first step is understanding the spectrum of “passive” and “active” fund management, starting with index funds.

Index funds

The S&P 500 is an index of 500 of the largest public companies in the US. An index is like a list of directions for an index fund, showing which stocks it needs to own and in what proportions. An index fund is committed to matching the index portfolio regardless of its performance. The managers can’t decide to change the portfolio because they think they can pick a better one.

The first index funds were launched in the 1970s, but didn’t pick up significant assets until the 1990s. Since then, index funds have grown from obscurity to more than half of money managed by US funds. Most prominent indices are created and maintained by specialized companies like S&P Dow Jones, MSCI, and FTSE Russell (say it like “footsie”).

Trillions of dollars follow the S&P 500 alone — more than any other index. There are a number of S&P 500 index funds, managed by different companies. Funds have tickers just like stocks, so we can refer to them concisely with the ticker. The S&P 500 fund managed by Vanguard is VOO. Its counterpart at BlackRock is IVV.

Remember, a company’s market cap is the total value of its shares. The S&P 500 and many other indices are market cap-weighted (often abbreviated to just “cap-weighted”). What does that mean?

As I write this, the market cap of Netflix is $418 billion and the market cap of Domino’s Pizza is $15 billion. Let’s say you buy shares of an S&P 500 index fund, which contains both companies’ shares. You effectively own the same fraction of each company in the fund — maybe one billionth for a small investor. But Netflix is 28 times more valuable, so 28 times more money from your investment is allocated to Netflix than Domino’s. If Netflix shares rise by 3%, that affects the fund’s performance a lot more than if Domino’s shares rise by 3%. Market cap weighting is not the only way funds weight different stocks, but it’s the most common because it allocates dollars in proportion to the opportunity set. In other words, you buy more Netflix stock because there’s a lot more Netflix available to buy.1

Investing in an index fund is often called “passive investing”. The fund managers are indeed passive — they’re tracking an index. But the index provider (who designs the index and updates it over time) isn’t a passive actor. Your decision to buy or sell a particular index fund isn’t passive either. We’ll come back to that.

If a fund doesn’t track an index, it’s “actively managed”. Managers of these funds have varying degrees of freedom in their investment decisions. In some funds, the holdings are dictated by the personal judgment of a small team and ultimately by one person. You might buy a fund like this because you think the manager is uniquely talented. Peter Lynch, who ran Fidelity’s Magellan Fund from 1977 to 1990, is the most famous case of a star manager. In other funds, personal discretion is limited because they pursue a systematic, quantitative strategy. You might buy this type of fund because the strategy itself appeals to you.

Active funds typically benchmark their performance against an index. They may choose a reasonable index based on the universe of stocks from which they’re selecting. Some funds deliberately pick an index that they think will be easier to beat than a more appropriate index.

Winners and (mostly) losers

Let’s pose a question that will start narrowing our options: is there a difference in the distribution of returns you can expect from active funds and comparable index funds? Yes.

There’s a multi-decade history of academic research on this topic, which I’ll outline in a footnote.2 But some of the clearest measurements of active fund performance are in the SPIVA reports from S&P Dow Jones. The SPIVA US Scorecard periodically catalogs the performance of active US funds (i.e., funds available in the US, not funds that invest only in US securities). They compare active fund returns to a reasonable index benchmark, based on the kind of stocks or bonds that each fund holds. One way to categorize funds is by market cap. Companies are sorted by market cap with the standard labels “large cap”, “mid cap”, and “small cap”. If an active fund invests mainly in large cap US stocks, they benchmark it against the S&P 500. Comparisons range in duration from the prior year to the prior 20 years. How do active funds measure up to their passive counterparts?

When compared in the last year, the portion of active funds that underperform their benchmarks are all over the map. Usually more than half underperform, but depending on the category and the year, underperformers have been as rare as 9% and as common as 99%. As we extend the time period and look back further, the pattern clears up. More and more funds fall behind their benchmarks in the long run. The figures shift each year, but overall about 90% of active stock funds underperform their benchmark over the prior 20 years. Active bond funds have a better record, but the median active bond fund underperforms its benchmark in every bond category.

That looks bad for active management. But these figures aren’t entirely fair: the best funds tend to grow large, so most of the money is in the larger, more successful funds. A simple count of underperforming funds won’t give us the whole picture. To address this, the SPIVA report provides asset-weighted average returns: funds are factored into the average by assets under management. This provides a better view of how money fares under active managers.

Over the last 20 years, US large cap funds had an average annual return of 8.48%. But there are a lot of small funds with poor performance. Weighted by assets, these funds returned 9.09% per year. That’s much better! But the S&P 500 returned 10.35% per year, and 92% of these funds underperformed it. The S&P 500 has been unusually difficult to beat in recent years. But the same pattern applied to nearly every category of stocks.

Active bond funds are a significant counterpoint. Over the last 20 years, investment-grade intermediate funds returned an average 3.42%, against a benchmark of 3.01%. But the index for another category (general investment-grade funds) beat the active managers, 4.12% to 3.20%. Bond funds are a mixed bag, which is interesting because stock funds tell a more uniform story of failure.

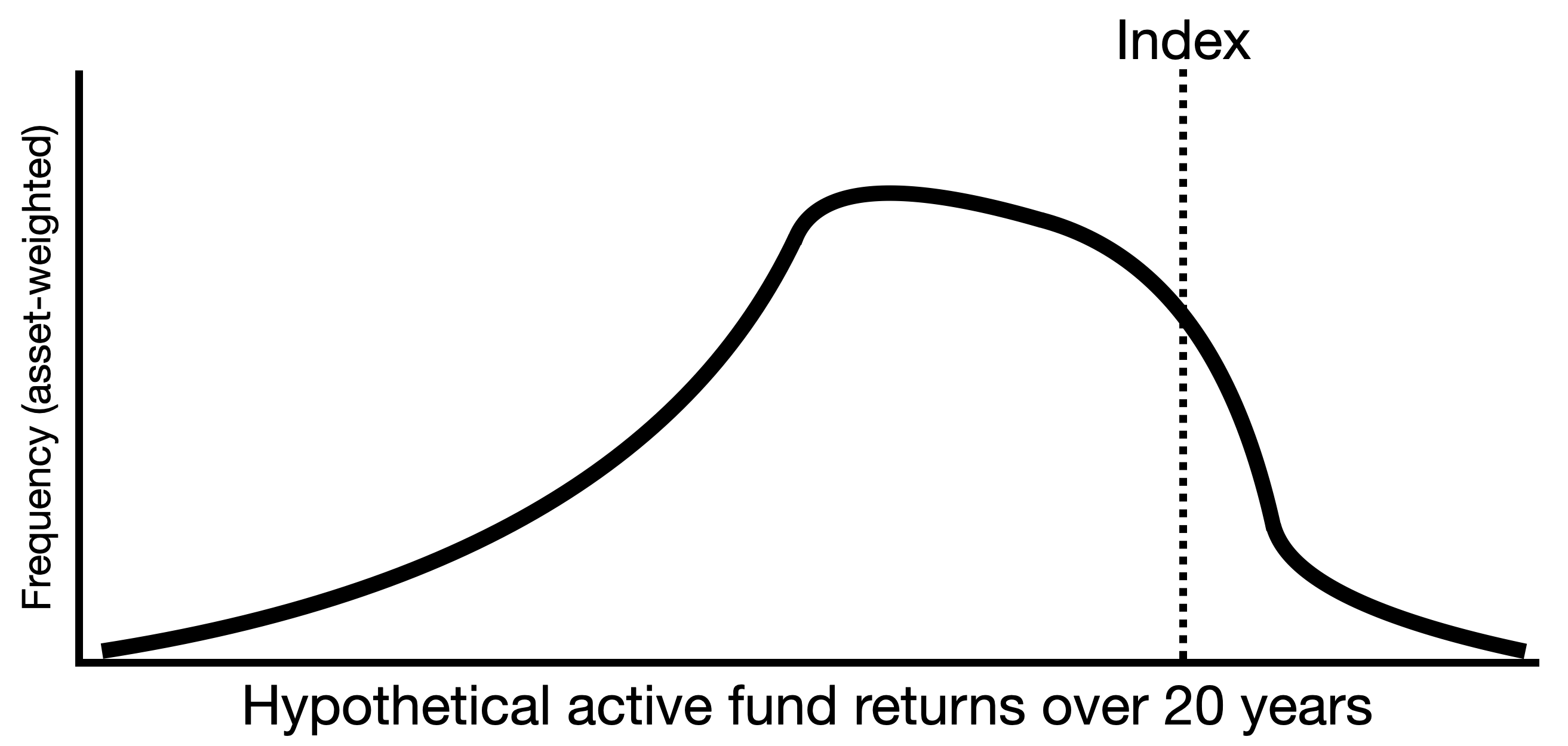

Long-term active fund performance is a negatively skewed distribution. Here’s a toy diagram I made illustrating how that distribution might compare to its benchmark. Most returns are worse than the index, and some are much worse. A small portion of returns slightly exceed the index, and another small portion significantly exceed it.

An attentive reader might see this and ask: okay, 90% of active stock managers lose to a non-sentient list of stocks. Why don’t we buy some funds in the top 10%?

If you’re able to identify them in advance, you can! This would transform a very difficult task (picking stocks on your own) into a less difficult task (picking managers on your own). I suppose that’s progress. But another report, the SPIVA Persistence Scorecard, addresses the difficulty of recognizing successful funds before they put up great returns. There’s no consistent layer of top performers. Most funds in the top 25% over any period of five years fall out of the top 25% over the next five years. This holds in the last five years and the five years prior. As you can infer from the data we explored above, many funds in the top 25% still fail to beat their benchmarks.

But why?

Good question. Why are there so few active stock funds that outperform a fair benchmark in the long run?

Fees are higher in active funds, putting any active manager at a disadvantage compared to low-fee index funds.

Reducing diversification is more likely to result in underperformance than overperformance.

A great deal of temporary outperformance is due to luck, and the role of luck decays over time (although much more slowly than most people would think). Underperformance, whether due to bad luck or not, is often swept under the rug by shutting down funds and opening new ones.

The most successful funds over short periods tend to be those that embrace an investing style or sector that happens to perform well. Fortune eventually stops smiling on such funds when that style’s time passes. This is a form of luck, but it’s worth identifying.

Active managers are mainly competing against and trading with other institutional investors. What matters is not whether the managers are highly skilled and equipped with deep resources — many are — but whether they can continually outcompete other active managers. Like any competitive sport, investing is a game of relative skill.

Managers who exhibit signs of skill are quickly buried in money. If you’re managing a $50 million fund, you can use a small number of your best ideas. But success brings excited new investors. Once you’re managing billions of dollars, you have to spread the money across an increasing number of investments, and your best 200 ideas can’t be as good as your best 20. Larger funds can also suffer from higher trading costs (moving prices more as they trade in size).

Some managers with exceptional performance make a ton of money and retire young, leaving someone else to manage the fund. The replacement may not be as talented.

Fees, killer competition, and diminishing returns with size are key reasons for active underperformance. Exceptional skill in money management is real, but it’s challenging to identify in advance because so many investors are competing to place their money in the right funds.3 A manager with talent disproportionate to the size of their fund is like an undervalued stock. The most skilled manager can be undesirable due to an oversized fund, and a high-quality company can be a bad investment if the stock price is too high.

In addition, a big-picture idea called market “efficiency” is crucial to explaining the difficulty of beating passive approaches. It’s often misunderstood and deserves its own post. For the moment, we can recognize the impressive and counterintuitive track record of just buying a broad index.

Play dead

If you consider what I wrote above, you could still decide to pick active funds or select your own investments. I don’t say that no one should do that, as long as you appreciate the dynamic between active and passive investors, and the extra time and stress demanded by active management. But I can’t say much about active investing because there are unlimited ways to do it.

So let’s assume, for the sake of continuing, that we’ve accepted the arguments against buying active funds. We still seem to have a lot of work ahead of us. There are thousands of index funds! How do we use them to capture the benefits of passive investing? At its core, investing “passively” means that we implicitly choose to accept market prices, so we do not favor some stocks over others.4

Many funds track an index that is active in spirit. Invesco, for instance, manages a fund that holds solar energy companies based on an index. Shareholders of this fund are deciding to hold a few dozen companies, and the humans creating the index have to make decisions about which companies to include and how to weight them.

So a fund can effectively pursue an active strategy by following an index. And as we’ll discuss later, a fund can be strongly governed by rules without tracking an index. The terms “active” and “passive” are a much better description of fund managers than fund shareholders. Adriana Robertson has pointed out that portfolio construction is decided either by the portfolio manager (in an active fund) or by the index provider (in a passive fund).

Okay, back to searching for a passive index fund. What about the S&P 500? A lot of people buy an S&P 500 index fund like VOO and consider themselves passive investors. Beyond requiring companies to exceed a market cap threshold — the S&P 500 is for large cap stocks — that index has a long list of eligibility criteria. It’s also limited to 500 companies even though more than 500 are eligible, so a human committee decides which companies are included. Even so, it’s a decent representation of the US stock market. And it’s not the only one: the Russell 1000 Index contains the largest 1,000 US companies.

But what if we want to passively buy the whole US stock market at market cap weights? That’s easy: a fund managed by Vanguard tracks the most comprehensive index of US stocks, the CRSP US Total Market Index. The ticker for this fund is VTI. (People rarely memorize the name of the index their fund is tracking, but many investors can recognize popular tickers like VOO and VTI.)

But whether we buy 500 US stocks or 1,000 or all of them, we’ve still excluded every stock from the rest of the world. You may favor the US market or not, but deciding to hold only US stocks is an active decision. I said passive! What if we want the cap-weighted global stock market? That’s easy too: another Vanguard fund tracks the FTSE Global All Cap Index (don’t forget to say “footsie”). Its ticker is VT. This fund still mostly holds US stocks, because the US stock market is currently over 60% of the global market.

As mentioned above, “passive” and “active” investing is not a dichotomy. The solar energy fund is highly active; VOO is somewhat passive; VTI is slightly more passive; and by our definition, VT is the most passive single fund for someone buying stocks. So does buying VT make us a passive investor? Let’s think about the ways in which it does and does not.

If we bought shares of a fund that overweighted some stocks relative to market cap weights, that would express a belief about which stocks are likely to be better investments. By purchasing shares of a fund that contains all stocks at market cap weights, we’re deliberately not overweighting or underweighting any stock. We’re assuming that the market price is the best guess we can get for the fair price of each stock. (We’re not assuming that market prices are judged perfectly or anything close to that.) In that sense, we’re a passive investor.

But everyone has to decide how much money to save for their investments. They decide how much to invest in stocks and in bonds (as well as which types of bonds). They have to select specific funds. They have to decide how much money to invest in each fund, and how often. They also have to decide when to sell shares. Or if they don’t want to make these decisions, they can outsource some of them to a financial advisor. But they’re still ultimately making the decisions because they picked their advisor and could switch to another one with a different approach at any time.5

In all those ways, everyone is an active investor. You can’t avoid consequential decisions, and there is no default option most of the time. Despite that, investing can still be extremely simple.

There’s so much more to say, but I would hate to say too much at once. We’ll cover a bunch of practical material in Part 3. See you next week.

Further resources

Every Money IRL post is organized in The Omni-Post, and all vocab terms are here.

I made a low-effort meme for this post but all I did was link to it, do you wanna see it??

The Rational Reminder interview with Jonathan Berk and Jules van Binsbergen explains a ton of ideas about fund managers and investors that I touched on above. You’ll understand this post much better after watching or listening to it.

I linked to a Rational Reminder interview with Adriana Robertson in the main body, which I recommend watching for great points on why passive investing entails active decisions by multiple parties. She wrote a paper on this, “Passive in Name Only”.

A summary of all three parts of the gentle intro to investing is here.

For a well-researched and interesting book on the rise of index funds, check out Trillions: How a Band of Wall Street Renegades Invented the Index Fund and Changed Finance Forever by Robin Wigglesworth.

—

We love comments here. Tell us what you like or dislike, agree or disagree with. Recall a long story barely related to this post. Ask a question!

Please send photos of your pets if you’d like to see them in future posts. Or suggest a new topic, or say hi! You can email or tap the message button. Stay safe out there.

Email: bright.tulip711@simplelogin.com

—

Weighting by market cap also minimizes the need to trade. If Netflix shares were to fall by 12% in a given quarter, its market cap would fall by roughly the same degree. To match the updated index weights in the following quarter, a cap-weighted index fund would need to buy or sell very few shares. If an index fund weights its holdings by some other method, more trading is required, incurring more trading costs.

Two distinct questions we can ask are: (a) Do some managers outperform due to skill, not just luck? and (b) Do some funds have persistent outperformance due to skill? Many people have conflated these questions, as explained in footnote 2. A few major papers on this topic (among many) are Carhart (1997), Berk & van Binsbergen (2015), and the two papers with conflicting results that Harvey & Liu (2022) attempted to resolve: Kosowski et al. (2006) and Fama & French (2010). My own takeaway is that manager skill clearly exists, but exceptional skill often doesn’t lead to persistent outperformance (due to reasons in the bullet point list above). Identifying funds that will outperform in the future is difficult, because there’s a competitive market for skilled managers that chases excess returns to zero. The market appears to be less competitive for bond fund managers than equity fund managers.

Berk & Green (2004) wrote a highly cited paper arguing that fund investors are fairly rational, as shown by their inclination to pile into successful funds until managers can no longer achieve excess returns. They developed a detailed model for investor and manager behavior. Despite Berk and Green’s clear explanation, even experts like Harvey & Liu (2022) write that “Skill in our context is measured by after-fee excess returns.” They’re measuring excess returns for investors, not manager skill. Skill should be measured based on value extracted: fund size multiplied by gross alpha (excess return before fees; Berk & van Binsbergen, 2015).

This isn’t the only conclusion one could reach after deciding to accept market prices. We’ll discuss a more sophisticated (but not necessarily better) approach in the future.

There’s a general version of this problem: many people think you can outsource your opinions to experts. But experts are unanimous on very few topics, so “deferring to experts” is more honestly phrased as “deciding which experts you find most credible”. If you hire an advisor in part because you want to outsource investing, you aren’t “trusting the experts”. Whether you knew it or not, advisors have different approaches, so you selected your investment approach when you selected your advisor. On top of this problem, most financial advisors aren’t experts in portfolio management.