You should probably have more auto insurance - even if you don't drive! (part 2)

But don't pay more than you need to.

In Part 1 of this post, we discussed the main types of coverage you should consider on your auto insurance policy. With that foundation, we can move on to some big-picture topics.

What if you don’t have a vehicle?

If you don’t own or lease a vehicle, or don’t even drive, you still live in a world where humans — one of the great apes, may I remind you — operate multi-ton hunks of metal at high speeds. You can be struck as a pedestrian or cyclist, or as a passenger in someone else’s vehicle. And if you borrow someone else’s car, or rent one — however rarely — you’re exposed to all the liability risks of a regular driver.

So what coverage should you buy as a non-owner?

UM/UIM bodily injury coverage compensates you for injuries caused by uninsured drivers, as well as hit-and-run drivers. Everyone should have this coverage. Unless you live in Antarctica, everyone is a pedestrian in proximity to cars at some point. And almost everyone is a passenger occasionally.

Liability coverage protects you against lawsuits if you’re deemed to be at fault for a collision. If you never drive, then you can skip this coverage, but anyone who might drive in the next six months should add this to their policy.

Medical payments coverage can supplement your health insurance if you’re in an accident. It isn’t essential, but the price is so low that you should consider adding it. If you live in a state that requires personal injury protection (PIP) coverage for drivers, you may want to buy PIP coverage for yourself. If you’re injured in a crash as a passenger, the driver may not have enough PIP coverage for everyone in the vehicle. State minimums for PIP coverage are often paltry — and many states don’t require first-party medical coverage at all.

How to buy auto insurance

It’s possible to buy auto insurance in about ten minutes online, and it renews automatically at a new (usually higher) price every six months. Getting the best price for the coverage you want takes a little more work.

My personal rule is that I shop around for auto insurance (a) every two years or (b) whenever I move to a different zip code. Checking more frequently is usually a waste of time. But price comparing will show you why it’s worth doing occasionally: I’ve received a quote from one major insurance company up to four times as expensive as a quote from another. You can earn thousands of dollars of savings with one or two hours of menial work. I also gather a few quotes before buying a vehicle, to avoid being surprised by the new insurance rates.

I shop for the best price with the ten largest auto insurers, as well as a few regional companies that I find by searching for “best” or “cheapest” auto insurance in [my state]. I also email a couple independent brokers with my desired coverage, and they find the best price available to them. Even from the same insurance company, the price available to an insurance broker may be higher or lower than the price offered to me when I directly apply for my own quote. So it can be worth using both methods. The best price for me has always been through Progressive, but pricing is highly dependent on the individual, vehicle, and location. The only way to know for yourself is to check.

All licensed drivers in your household should be named on the policy. You can inquire about excluding a driver from the policy, but it may not be possible depending on the company and your state. If you don’t name all the appropriate drivers, you could be in violation of your contract and your insurance company could return your premiums and reject coverage at any time — including when you try to make a claim.

Before shopping for quotes, have the VIN for each vehicle and the license number for each driver ready to copy and paste. Do the same with your email address, phone number, and residential address. You’ll have to enter them for each quote.

Yes, it’s tedious work, but you can do it efficiently in a couple hours every two years and potentially save yourself a lot of money.

How to pay less for auto insurance

There are a few easy and quick ways to lower your auto insurance premiums. Shop around for the best price, and save 5-10% by paying up front for all six months of a policy. If you can’t afford to pay for six months at once, that’s a sign of a deeper cash flow problem. You can ask your insurance company about ways to pay less. There are discounts in some states for taking an online defensive driving course (which mostly involves letting videos play and taking easy quizzes). If you’re a student or there’s a student driver on your policy, ask about discounts for good grades. GEICO has a discount for Berkshire Hathaway shareholders! You might save by bundling multiple vehicles or policy types with a single company.

The other ways to pay less are not so simple. Your premium largely reflects the risk perceived by your insurance company. Risks are partly due to your location: how frequent are accidents in your area, and how expensive are they? How many drivers are uninsured?

But the other risks are presented by the drivers on the policy. Your driving record in the last several years is a central factor: How many claims have people on your auto policies made, and how many were at-fault accidents? How many tickets do you have for speeding and running red lights? Do you have a DUI or DWI conviction? How many years of driving experience do you have? How many miles do you drive annually?

Those are all core data points that an insurance company uses to predict the risk you pose to their business. You may not agree that a few speeding tickets make you more likely to be in an accident, but their highly informed view is that you are wrong.

As a whole, younger drivers are greater accident risks, so their premiums are higher. To a lesser degree, the same goes for male drivers relative to females. Married people, homeowners, those with higher credit scores, and those with higher formal education tend to be charged lower premiums.

You might again bristle at the unfairness. Men are charged more than women just for being men?? Some states agree with you, and forbid insurance companies from using gender or credit score to calculate premiums. Some states even restrict the use of age, driving experience, or location. But that comes at a cost: in those states, female drivers effectively subsidize the premiums of male drivers, and those with high credit scores subsidize those with low credit scores. In other words, safer drivers subsidize more dangerous drivers because state regulators insist on it.

Once you understand the rules, you can work them to your advantage. Obviously: don’t speed excessively, don’t run red lights, and drive like a reasonable sane person. Don’t ever let a fine go unpaid — pay it promptly. If you have a moving violation or an at-fault accident in recent history, all you can do is wait for them to fall off your record and drive better from now on.

The same goes for your credit score: if you have a low score now, you can greatly improve it in a few years. Make sure you have at least one credit card, and set it to autopay the statement balance every month so that you never miss it. If you can’t qualify for a credit card, apply for a secured credit card first. Always pay your debt on time, don’t ever not pay your debt on time, and your credit score will rise. All else equal, a higher credit score makes you a lower risk in the eyes of an insurance company.

If your collision and comprehensive premiums bother you, you might be able to lower them by switching to a car that doesn’t cost an arm and a leg to repair. You need to anticipate before you buy a vehicle that insurance is a large portion of the long-term cost, and check the current insurance rates. I own a base model Subaru Crosstrek partly because it’s a common, reliable vehicle with reasonable repair and maintenance costs. It was only $25K new, so if it were totaled, replacing it wouldn’t cost my insurance company a fortune. That feeds into lower collision and comprehensive premiums for me.

There are some things you can’t change. If you live in an area that’s dangerous for cars, your insurance premiums will be relatively high. You can reduce the likelihood of some incidents by parking your vehicle indoors and taking public transportation when possible, but you can’t make a major city as safe as a rural town.

My heart goes out to anyone paying for a teenage driver. If they start driving early, insurance companies will eventually note that they have significant experience. With a good record, you can expect major price declines throughout their 20s. However, the most important part of this process is deciding when they’re ready to drive on their own. Teenagers are slapped with sky-high insurance premiums because, as a group, they’re extremely dangerous drivers! Although driving is an important skill, parents do not have an unquestionable obligation to put themselves at risk of lawsuits in order to help their children become drivers as soon as possible. Some kids are not ready to drive alone at 16.

If you have a poor record, it may not be feasible for you to max out your coverage like I’ve suggested. That’s not the end of the world — hopefully — but you should work on lowering your premiums so you can afford to gradually increase your liability and uninsured motorist coverage.

Get a dash cam. Your insurance won’t give you a discount, but it protects you by furnishing a nearly indisputable witness at the scene if the other driver was at fault. Without one, it may be your word against theirs. You can also avoid becoming a victim of premeditated insurance fraud. And you might just catch some interesting footage. I use this dash cam with this memory card. You don’t need anything fancy, but I do recommend installing front- and rear-facing cameras. You can follow this video to install it yourself, or visit a professional shop and pay them to do it. Installing the rear-facing camera can be a pain, so if you’re procrastinating, just hire a pro and get it done for your own safety.

Bring an umbrella ☂️

Car accidents can happen suddenly, with high-stakes decisions demanded of you in a split second. Under these conditions, anyone might take action that leads to them being deemed partially or wholly responsible for an accident. The cost of these accidents can exceed even the largest policy limits for auto insurance.

Take the following scenario:

You’re driving on the highway in heavy rainfall, and you briefly lose control of your car. It drifts into the next lane and collides with another vehicle, causing the other vehicle to roll multiple times. You’re able to pull over without physical injury. Based on another party’s dash cam footage, you’re deemed to be 100% at fault.

The other car was totaled; its cash value was $50,000. The driver and passenger were both injured by the crash. They’re a dual physician couple, each earning a salary of about $400,000. The husband was out of work for a month, the wife for eight months. Her injuries required a surgery and extensive physical therapy. They sue you for the medical expenses, lost income due to not working, and pain and suffering, to the tune of $900,000.

If you had collision coverage, you would pay your deductible and your car would be repaired by your insurance.

Let’s say you have a 250/500/100 liability policy. Your insurance will pay to replace their car, because the value is less than the $100K property damage liability limit. But what about that $900K lawsuit for bodily injury liability? Let’s say the husband’s portion of that is only $150K. Your policy’s limit is $250K per person, so insurance will pay a total of only $400K. If they aren’t willing to settle for your policy limits and decide to pursue you personally, you’re on the hook for the remaining $500K — good luck.

Is that an extreme example? Yes, you’d have to be unlucky to find yourself there. But it’s a representation of terribly expensive lawsuits that happen all the time. Don’t take my word for it: as mentioned in Part 1, Michigan warns every driver about the severe financial risk of choosing low bodily injury liability limits.

But what if you buy the most liability insurance offered, and someone sues you for even more than that? Many (but not all) insurance companies offer maximum bodily injury liability of $500K, and offerings differ by state.

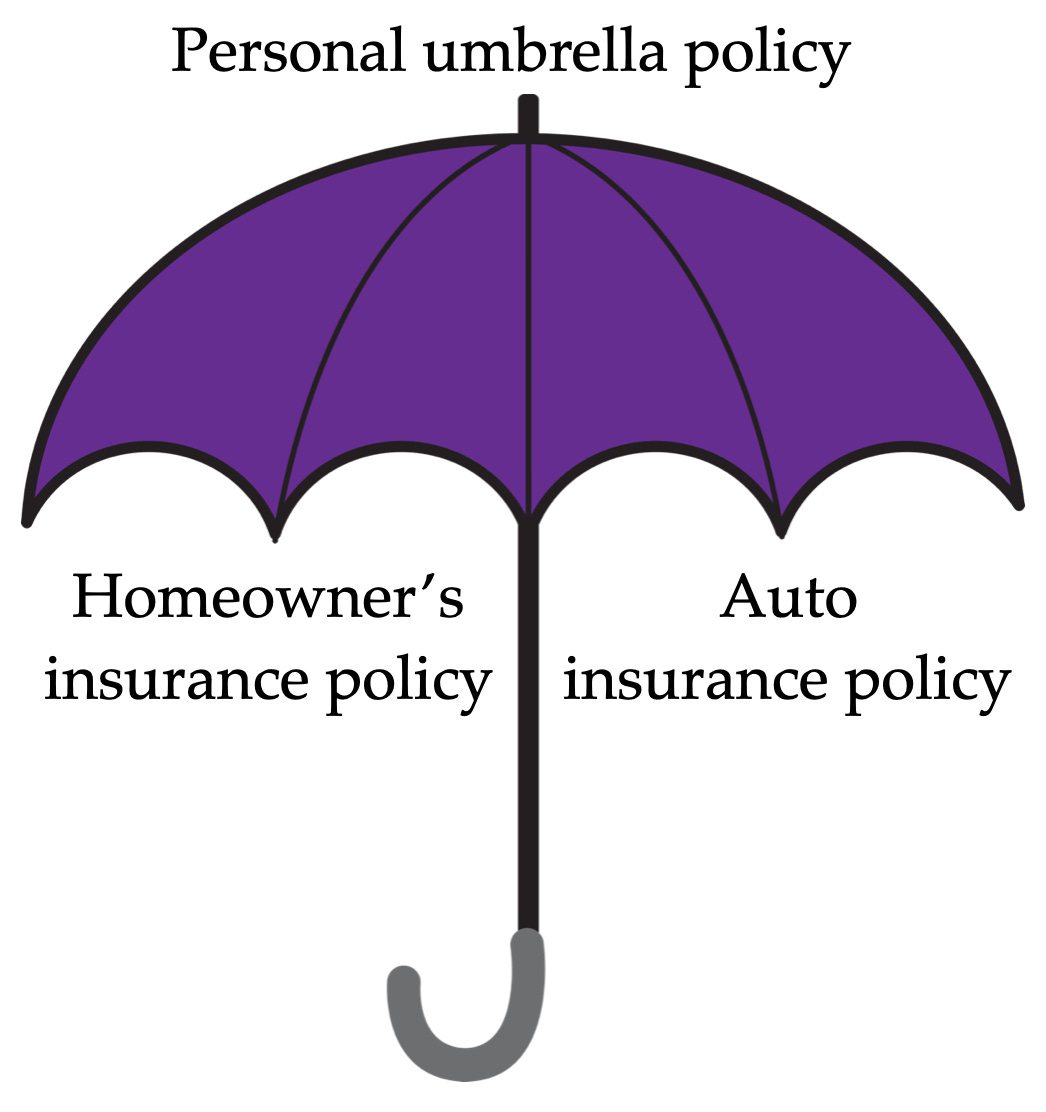

That’s why I suggest considering a personal umbrella policy. An umbrella policy stacks on top of the liability coverage of your auto and homeowner’s insurance (including renter’s insurance), and protects you in case your liability exceeds the limits of either policy. It also covers personal liability more broadly, including defamation suits and liabilities you incur outside the US. In the case above where your auto liability coverage was exhausted, an umbrella policy would pay the remaining $500K and your personal assets would be untouched.

Because they’re rarely needed and only expand liability coverage, umbrella policies are cheap. Along with the new auto and renter’s insurance policies I bought when I moved to Colorado, I bought a $1 million umbrella policy. I paid a premium of $270 for a year of coverage, which is $22.50/month for a MILLION DOLLARS of liability insurance covering both me and my partner. That’s a lot of protection and peace of mind for less than premium Netflix.

Of course, your umbrella policy could cost more than mine. It probably will if you have risk factors like a pool at home or a personal boat. Public figures are at greater risk of liability and defamation lawsuits. You should still think about buying it.

Along with your umbrella policy, you may have the option to buy additional UM/UIM coverage. I was quoted $352 (about $29/month) for another $1 million of coverage, which I decided not to purchase.

Your umbrella policy doesn’t need to be with the same company that provides your auto and/or homeowner’s insurance.

On top of the raw numeric increase in coverage, it’s worth considering the incentives of your insurance company. If you carry the state minimum coverage and you’re deemed at fault for an accident, they don’t have reason to spend much on legal fees for you. Let’s say your liability coverage per person is $25K, and you’re being sued by one person. At most, the insurance company will pay $25K if the lawyers lose your case. Should they spend many thousands on legal fees for a chance at slightly reducing the payout or, at best, not paying $25K? From their perspective, you’re a peasant. Your case is not worth significant resources.

But let’s say you have a 250/500/100 auto policy, plus a million dollars of umbrella liability coverage. Now they could lose well over a million dollars. They’re incentivized to do everything they can to minimize the settlement or court awards, because they’re picking up 100% of the bill.

Buying a lot of coverage aligns you with your insurance companies. You want them in your corner.

Summary of Part 2

Even if you don’t drive, you should have UM/UIM bodily injury coverage at the very least.

Shop around on your own and work with an independent broker to find the best price.

Understand how insurance companies decide how much to charge you, and make yourself a lower risk.

Buy a dash cam and install it promptly.

A personal umbrella policy completes your insurance package, providing a lot more liability coverage at low cost (for most people).

See you next week!

Further resources

Every Money IRL post is organized in The Omni-Post, and all vocab terms are here.

Check out this video by Two Cents on ten ways to lower your auto insurance premiums.

The Reddit forums r/dashcams and r/IdiotsInCars are good ways to convince yourself to buy a dash cam.

Here’s a dash cam video of a group of people attempting insurance fraud by manufacturing a rear-end collision.

Here’s a great tutorial video by ChrisFix on how to install a dash cam.

You can only hope to have a dash cam setup as nice as this one, which this driver used to document his criminal activities. Really though, it’s a great three-channel setup and must have cost him $300+.

There are several good links — none of which are about dash cams — in the further resources of Part 1.

—

We love comments here. Tell us what you like or dislike, agree or disagree with. Recall a long story barely related to this post. Ask a question!

Please send photos of your pets if you’d like to see them in future posts. Or suggest a new topic, or say hi! You can email or tap the message button. Stay safe out there.

Email: bright.tulip711@simplelogin.com

—